Financial literacy isn’t really about balancing a checkbook or memorizing the rules of a budget. It’s about opportunity — the ability to make informed choices, avoid costly mistakes, and steadily build the kind of stability that lets a family move up rather than just hang on. And across the United States, far too many students grow into adults who never got the chance to learn it. The cost shows up in individual households, but it ripples outward into entire communities and the wider economy.

Here’s what the evidence says, and why classrooms are the most powerful place to change it.

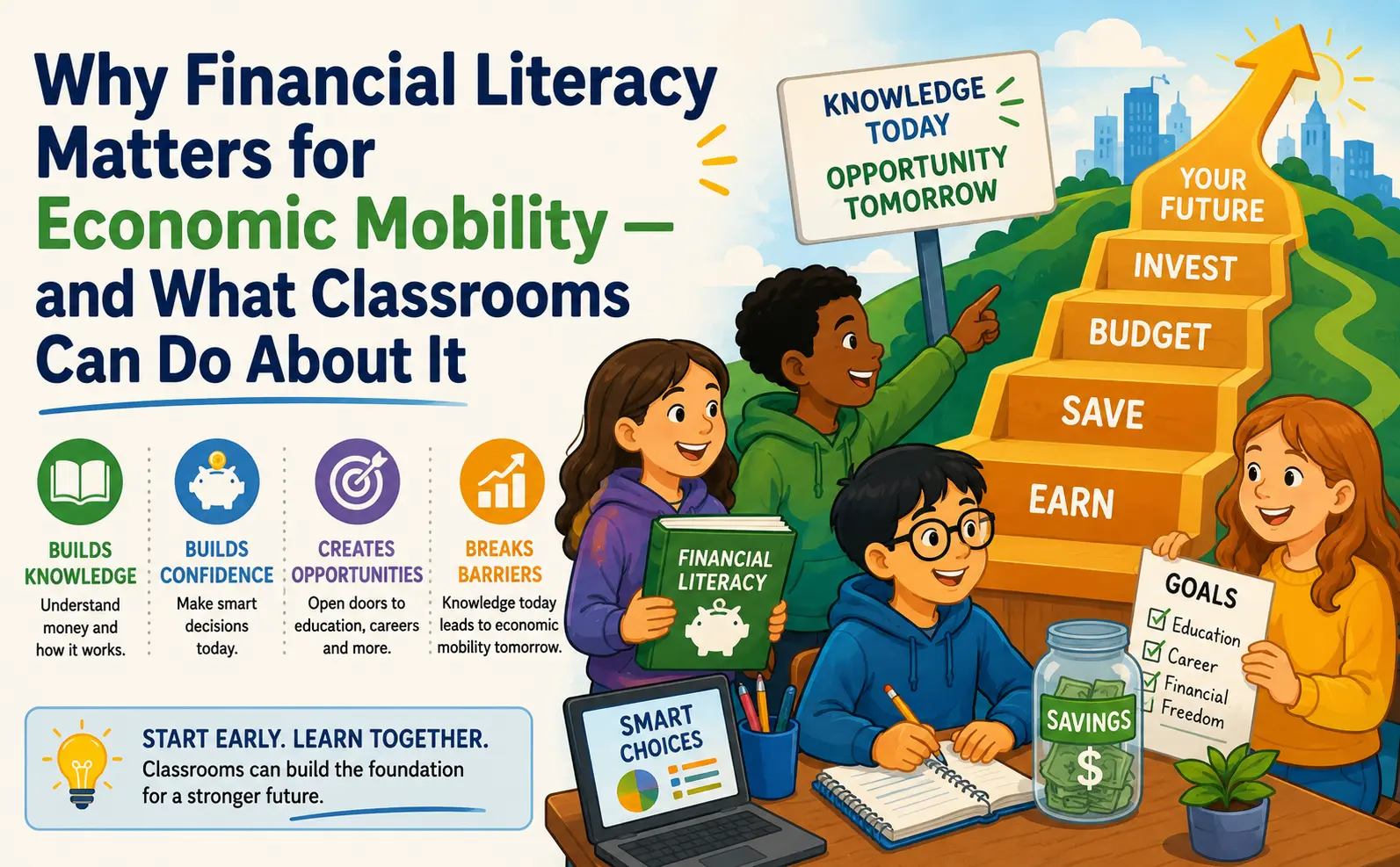

1. Financial Literacy Is Low — and It Isn’t Getting Better

For nearly a decade, researchers have measured how much American adults actually understand about money, and the answer has barely budged. On the most recent Personal Finance Index, U.S. adults answered fewer than half of basic financial questions correctly — a figure that has never climbed above 52% in ten years of tracking.¹ The youngest adults fare worst of all: Gen Z answered only about 38% correctly, entering adulthood with the thinnest financial foundation of any generation studied.¹ This isn’t a knowledge gap that’s quietly closing on its own.

2. The Real Cost Is Lost Opportunity

Weak money knowledge doesn’t stay abstract — it follows people into their bank accounts. Adults with very low financial literacy are roughly twice as likely to be constrained by debt and three times as likely to be financially fragile, meaning a single unexpected expense can tip them into crisis.² Without an emergency cushion or an understanding of how credit works, these households lean more heavily on high-cost borrowing, and money that could have gone toward education, a home, or a small business gets spent servicing interest instead. The opportunity that never gets funded is the real price.

3. Shaky Money Knowledge Locks In the Wealth Gap

When financial understanding stalls, so does mobility. People who don’t have a working grasp of credit, interest, and compounding are far less equipped to build the long-term assets that move a family up the ladder. Those gaps fall hardest on low-income families and communities that have historically had the least access to financial education and affordable financial products — which means the divide tends to repeat itself from one generation to the next rather than narrowing.²

4. Education Works — and Schools Are the Leverage Point

Here’s the encouraging part: when students actually learn this material, their outcomes change. Studies tracking young adults through their credit records found that those who came up under a state financial-education requirement had measurably higher credit scores and lower delinquency rates than peers in states without one — with the benefit growing for each successive graduating class as schools refined how they taught it.³ Reviews of the broader research reach the same conclusion: school-based financial education improves credit outcomes and reduces the likelihood of falling behind on payments.⁴

Policymakers have noticed. As of late 2025, 30 states guarantee every high school student a standalone personal finance course before graduation, and broader counts that include embedded requirements run higher still.⁵ One analysis estimated the lifetime value of a single semester of high school personal finance at roughly $127,000 per student.⁶ Schools, in other words, are where the leverage is.

5. Why This Matters for Fun Banking Classrooms

At Fun Banking, we don’t think financial literacy is an enrichment activity to bolt on if there’s time left over. It’s a core life skill — and it sticks best when students practice it rather than just hear about it.

That’s the whole idea behind a classroom economy. When kids earn a paycheck, pay their bills, decide whether to save or spend, watch interest grow in a savings account, and feel what it’s like to carry a balance on a credit card, they’re rehearsing real decisions in a safe place where the stakes are pretend but the lessons are real. They learn that borrowing has a cost, that saving early pays off later, and that small choices compound — the exact concepts the research shows make the difference in adulthood. Teachers get a more engaged, more financially-aware classroom; students get a head start on the skills that shape the rest of their lives.

Final Thought

Economic mobility isn’t only a question of wages or job titles. It’s about whether someone has the knowledge and confidence to manage money well over a lifetime — to absorb a setback, seize an opportunity, and build something that lasts. Financial literacy is one of the most powerful tools a school can put in a student’s hands, and the earlier we put it there, the more it’s worth.

That’s why we built Fun Banking: to make hands-on financial learning something any teacher can run, starting tomorrow. See how it works or start free.

Footnotes

- TIAA Institute & Global Financial Literacy Excellence Center (GFLEC), TIAA Institute-GFLEC Personal Finance Index (P-Fin Index), 2026 ten-year findings. U.S. adults answered roughly 47% of index questions correctly, never exceeding 52% across a decade; Gen Z averaged about 38%.

- TIAA Institute, Financial Literacy and Retirement Fluency in America: Findings from the 2025 P-Fin Index. Adults with very low financial literacy were about twice as likely to be debt-constrained and three times as likely to be financially fragile.

- Brown, A., Collins, J. M., Schmeiser, M., & Urban, C., State-Mandated Financial Education and the Credit Behavior of Young Adults, Federal Reserve Board / FEDS Working Paper (2014; published in The Review of Financial Studies, 2016). Students under financial-education mandates showed higher credit scores and lower delinquency rates, with effects increasing for later graduating classes.

- Consumer Financial Protection Bureau (CFPB), A Review of Youth Financial Education: Effects and Evidence, 2019.

- Next Gen Personal Finance (NGPF), State of Financial Education and Live U.S. Dashboard, 2025 (30 states guaranteeing a standalone course); Council for Economic Education, 2026 Survey of the States (39 states requiring a personal finance course to graduate).

- Tyton Partners, Investing in Tomorrow: The Lifetime Value of Financial Education in High School.

Fun Banking is a classroom banking simulator — no real money, accounts, or financial services are involved.